Multinationals design and innovate new products and processes at a global scale and with advanced communications, development teams can be widespread across the globe with no real interruption.

However, the cost of developing and commercialising innovation and the underlying intellectual property is subject to different rules at local entity level. Consequently, it is important for decision makers to understand these local intricacies to better manage the cost of innovating as well as business profitability once the innovation is commercialised.

Building an innovation strategy based on an understanding of these principles is likely to yield much better post-tax outcomes than trying to retrofit partway through the development cycle.

Most European countries provide Government support for research and innovation with varying funding levels depending mainly on the types of projects and the size of the companies.

Innovation subsidies on ‘disrupter’ projects

These are usually granted after a competitive process and successful applicants receive funding throughout the project. Clearly, anywhere there is a competitive process, no applicant can be certain that they will be granted a subsidy so they are generally applied for and, hopefully, funding approved, before the R&D has been undertaken.

R&D tax credits

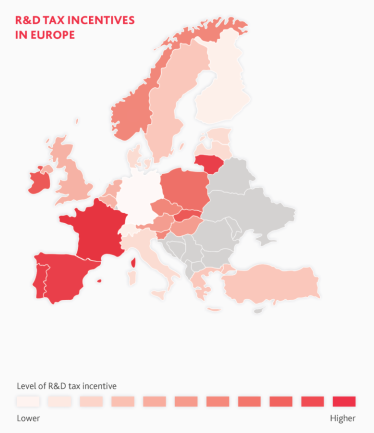

These tax credits encourage companies to invest in qualifying R&D by giving a tax deduction for a percentage of the amount of eligible expense of the project. To qualify, the R&D must increase the knowledge of the engineers or scientists in a particular field of engineering or science. Some countries offer the possibility of cashing the R&D tax credit even when the business is in a loss (so that, in effect, it acts as subsidy). The map below gives an overview of the current R&D tax credit regimes across Europe.

Patent/intellectual property box regimes

These result in lower effective tax rates being charged on income derived from certain qualifying IP. Patents and software copyrights qualify in most of these regimes but royalties, licensing fees, gains on the sale of IP, profits on the sales of goods and services incorporating IP, and patent infringement damage awards can qualify under some countries’ rules.

Doing the right thing in the right place

Understanding the different tax reliefs available in the countries in which you operate and the wider incentives offered is important to determine the net cost of development work as well as the cash flow in a global business. Therefore it is vital to map how the development and commercialisation of the IP happens in your business - answering the following key questions will help you start that mapping process:

- What IP is developed by the innovation process (both registered and unregistered)?

- Who generates and owns the IP, and who bears the associated risks (both funding risk and other legal or commercial risks)?

- Who are the strategic decision makers related to the development, enhancement, maintenance, protection and exploitation of the IP and where are they located?

- Is the location of the strategic decision makers different to the location of IP ownership?

- What does the commercialisation model look like?

- What is the overall governance framework and how is it formalised from a legal perspective?

- What method of intragroup pricing is used? Analysis of the role of each entity within the group and the nature of intra-group recharge such as royalty-based or cost plus mark-up etc. is vital.

- What is the accounting treatment of the IP/work done?

Even when you have mapped your IP landscape within the business, modelling and planning investment in R&D can remain a complex process often with many trade-offs to be managed. Of course, regular review of your structures is also important as the rules in different countries often change or are updated.

BDO has member firms in 167 countries and routinely work in international teams to support global businesses understand these reliefs and incentives alongside wider tax implications of R&D investment.

Contact our local expert, Cathy Kelly, should you have any questions.

Subscribe to receive the latest BDO News and Insights

Please fill out the following form to access the download.